Zaid Kamhawi, CEO of Qarar, explores the key components of a digital banking strategy, and reveals the benefits for banks who commit to a full digital transformation.

A bank’s drive for digitisation is usually fuelled by its desire to improve profits from a combination of increased revenues and lower operational costs. In the coming years we can expect a large part of global banks’ revenues and profits to come from lending to personal and small and medium enterprise (SME) segments. Through digitisation the lending pie can be expanded many times thanks to vast ambient data. As research studies show, banks that successfully use digital technologies could achieve a 40% profit increase, but amongst the biggest drivers for digital transformation is the customer experience evolution. According to Forbes, 63% of consumers will pay more for a great experience — especially Gen Z customers that demand instant gratification and are willing to pay for it.

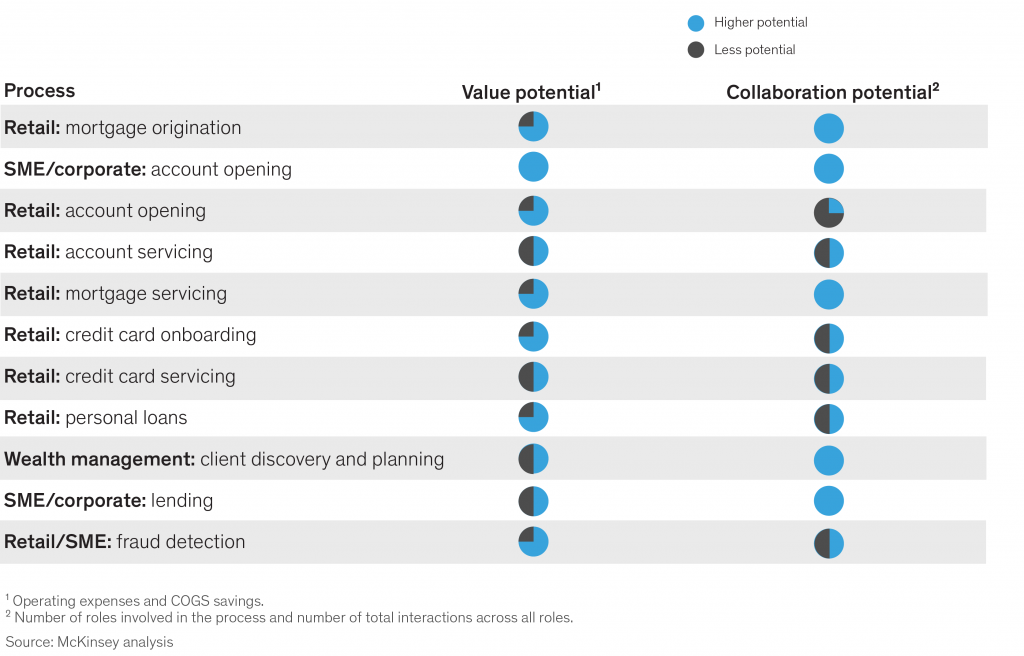

To achieve the desired level of digital proficiency requires a combination of advanced analytics as well as process automation. It also equally requires the digitisation of customer-facing touchpoints in addition to back-end business processes. According to a McKinsey analysis, mortgage origination, credit card onboarding and fraud detection are amongst the processes that hold the highest value potential in cost saving and productivity when digitised. This includes the automation of back-end process such as those used by underwriters and loan officers, so that they seamlessly process applications as they move towards closing. Meanwhile, the dependency on model development such as Risk models are key in pushing “automatic” decisions — especially in the grey areas of loan approval.

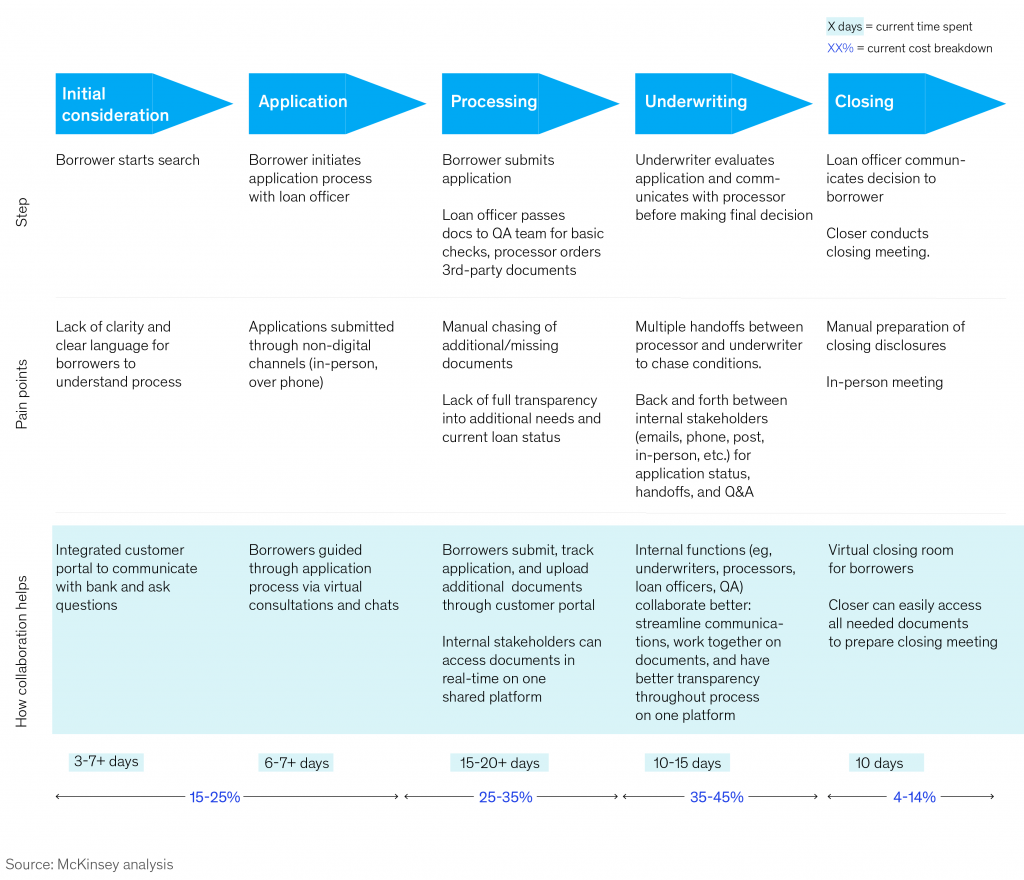

Digital collaboration can bring significant improvements to the mortgage origination process, according to research by McKinsey, as illustrated below:

When it comes to collateral-based lending such as mortgage origination, the current underwriting process can take 10-15 days and carries up to 45% of the origination costs with over 30 touch points and interactions. In Saudi Arabia, mortgages are also one of the retail banking sectors core products representing nearly 51% of total outstanding retail credit. Mortgages have also grown robustly in the GCC region in recent years largely thanks to a strong real estate sector. Digitisation of mortgages was already progressing in the region before the COVID-19 outbreak and the current crisis will accelerate and transform customers’ demand for digital credit. Leading banks have digitised the entire mortgage customer experience by establishing efficient end-to-end processing across platforms and all channels. The rewards can be significant. Known as the 150 rule, it brings a 50 percent improvement in the length of time to get a mortgage signed, a 50 percent reduction in bank costs and, most importantly, a 50 percent increase in customer-satisfaction levels. Again, according to McKinsey’s research, the potential benefits of collaboration increase with the frequency of communication, complexity of information, and number of decision points, as illustrated below:

While digitisation is having an impact on the lending value chain across all asset classes for retail and SME segments, the effect is particularly pronounced in unsecured lending. However, successfully digitising the lending process requires a digital interface that delivers instant credit decisions to customers, and that is supported by completely new underwriting criteria and risk processes. At its core, banks need an automated analytics engine that draws on hundreds of data points about customers — from external as well as internal sources — to support the loan-approval decisions. The other key element is a redesign of processes and a smart digital front-end workflow connecting the elements needed for smooth customer journeys and credit decision-making. For these fully automated applications, “time to yes” can be reduced from a window of 24 – 48 hours to just four minutes.

Advanced analytics has been enabling superior performance in organisations that are willing to make the proper commitment. Yet many firms also face a significant challenge in turning their analytics insights into business outcomes and realizing the full value of analytics, known as “attention to the last mile.” Many banks don’t even consider how the insights will be delivered, deployed and contribute to decision-making. This is where a bank needs to consider the workflow design and decision processes automation. This is why Qarar continually reminds the lending sector that every digital platform needs a powerful and robust decision engine in the background that can help it deploy its decision logic for any use case. For example, cross sell opportunities, fraud detection or credit risk underwriting.

To successfully capture the opportunities offered by digital collaboration banks can take several tactical steps starting with identifying those business processes that can be most improved through digitisation. Artificial intelligence (AI) has a big impact on banking. The banking industry will fully achieve digital transformation when AI is embedded and integrated into the range of applications and systems that support both back-office and customer-facing functions. Secondly, setting and electing the right technology roadmap, implemented in an agile way to identify early successes (digitisation of bank processes necessarily involves some trade-offs between cutting-edge technology and legacy systems). The banking sector has a long history of technology infrastructure. For example, in a survey by Cornerstone, 70% of respondents said that their institution’s current technology infrastructure was a barrier to digital transformation. Finally, a change management process to create adoption across the entire organisation — not only the executives at the top, the IT department or business managers — but everyone. Among the executives surveyed by Cornerstone, 85% said “corporate culture” was a barrier to transformation sparking the belief that maybe digital transformation in banking is not going to happen until the Gen Xers and Millennials dominate the executive committee.

If we were to take a quick snapshot of current global situation and digital banking potential, the influencing factors are clear to see. Software, technology, advanced analytics and digital know-how is readily available through Fintech experts such as Qarar. Customers’ expectations and service needs have already undergone a forced and radical transformation due to the COVID pandemic. Every business has had to adapt by embracing online transactions, back-office operations and a customer-centric focus as much as possible, purely to survive this ongoing global situation. The banking sector is no exception. Digital banking readiness can be measured by determination, focus and vision to take that bold step forward into the digital world — and the clock is ticking. Digitisation does not need to wait for next generation executives to future-proof their bank’s very existence. Because the leading banks are already making their digital transformation happen.